You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

The U.S. Economy: Stand by for more worse news

- Thread starter Brian Foley

- Start date

WASHINGTON July, 2008

—A panel of top business leaders testified before Congress about the worsening recession Monday, demanding the government provide Americans with a new irresponsible and largely illusory economic bubble in which to invest. "What America needs right now is not more talk and long-term strategy, but a concrete way to create more imaginary wealth in the very immediate future," said Thomas Jenkins, CFO of the Boston-area Jenkins Financial Group, a bubble-based investment firm. "We are in a crisis, and that crisis demands an unviable short-term solution."

"Perhaps the new bubble could have something to do with watching movies on cell phones," said investment banker Greg Carlisle of the New York firm Carlisle, Shaloe & Graves. "Or, say, medicine, or shipping. Or clouds. The manner of bubble isn't important—just as long as it creates a hugely overvalued market based on nothing more than whimsical fantasy and saddled with the potential for a long-term accrual of debts that will never be paid back, thereby unleashing a ripple effect that will take nearly a decade to correct.

The U.S. economy cannot survive on sound investments alone," Carlisle added.

"Every American family deserves a false sense of security," said Chris Reppto, a risk analyst for Citigroup in New York. "Once we have a bubble to provide a fragile foundation, we can begin building pyramid scheme on top of pyramid scheme, and before we know it, the financial situation will return to normal.

America needs another bubble," said Chicago investor Bob Taiken. "At this point, bubbles are the only thing keeping us afloat."

Here's some (unintentional) satire:

Paul Krugman 2002

To fight this recession the Fed needs…soaring household spending to offset moribund business investment. Alan Greenspan needs to create a housing bubble to replace the Nasdaq bubble.

Now Larry Summer's says we need a Bigger Bubble - which brings us right back around to The Onion.

Nearly 20% of the labor force is not working. 4 supporting. 1 Soon 3 supporting 1 if current trend continues.

For a broader long term view read: http://email.angelnexus.com/hostede...b694ba69830a938b2f582ed4c9c24191&ei=srz3QupwN But I advise a few stiff drinks first.

Last edited by a moderator:

Fed's plans:

** Because so many are getting discouraged and ceasing to look more for a job (see rapidly falling labor force participation graph of prior post) the Fed is in danger that its criteria for ending QEs will be met before it is safe (not very destructive to the economy) to begin the tapering. One solution to that is for example lower the 6.5% goal post to say 5.0%. Another is to offset the QEs ending with something that effectively also prints new money etc. but has a different name. - Called above "alternative actions."

Perhaps Fed should hold a name contest with $1000 prize for the winner? I don't think Fed is happy that many of us are calling QE3: "QEinfinity." If they do my entry is "TARP2."

* As I predicted at least 6 years ago.http://seekingalpha.com/article/1858771-the-fed-is-backed-into-a-corner?source=email_mac_mar_out_0_0&ifp=0 said:FED's FMOC participants discussed the wording that could be used in introducing the change and new promises that could be made in the Fed's forward guidance, while worrying that "communicating them could present challenges."

Among the thoughts expressed were that "it might be appropriate to offset the effects of reduced QE purchases by undertaking alternative actions to provide accommodation at the same time." Or that it could change its current forward guidance that it will keep interest rates near zero until unemployment falls to 6.5%, ** to a promise to do so until joblessness reaches an even lower level, which Chairman Bernanke floated in a speech this week.

Clearly, the Fed sees it has a problem as it moves toward actual tapering, if just the hints of tapering began to panic markets this summer. Meanwhile, conditions are not cooperating either. It had been expected that the unusual easy money policies would create rising inflation, and some inflation would be a positive for the economy. Early on, the Fed set a target of 2% as a limit above which easy money policies would have to be rethought.

However, inflation has inexplicably been declining instead, especially over the last 12 months. The Producer Price Index, measuring inflation at the producer level, declined 0.2% in October, and is up only 0.3% over the last 12 months. The Consumer Price Index, measuring inflation at the consumer level, declined 0.1% in October, and is up only 1.0% year-over-year. ... Meanwhile, deflationary concerns have also suddenly risen in Europe. It was reported last month that inflation in the eurozone was running at an annualized rate of just 0.7% in October, well below the ECB's target of 2%. The ECB reacted immediately by cutting its key interest rate from 0.5% to 0.25%, a record low.

Economists worry that the declining prices for goods in the eurozone are hurting business profits, weighing on hiring and business profits, and raising odds that the anemic eurozone recovery could slip back into recession.ECB President Mario Draghi said the ECB even discussed the possibility of setting interest rates at a negative rate (less than 0%) at its monthly meeting, an indication of the concern about deflation, and that he is under pressure to introduce a program of quantitative easing similar to that of QE in the U.S.

The emergence of a deflationary threat has to be an additional concern to the Fed as it considers when and how to exit its QE program. Hopefully, the Fed will find enough excuses in the economic and inflation reports, or on concerns about how Congress will handle its next chance to reach an agreement on a budget and the debt ceiling before the new deadline of January and February to keep the stimulus in place and markets positive through year-end and until April or May.

But evidence is piling up that 2014 is going to be an interesting year to say the least,* probably not at all like 2013.

** Because so many are getting discouraged and ceasing to look more for a job (see rapidly falling labor force participation graph of prior post) the Fed is in danger that its criteria for ending QEs will be met before it is safe (not very destructive to the economy) to begin the tapering. One solution to that is for example lower the 6.5% goal post to say 5.0%. Another is to offset the QEs ending with something that effectively also prints new money etc. but has a different name. - Called above "alternative actions."

Perhaps Fed should hold a name contest with $1000 prize for the winner? I don't think Fed is happy that many of us are calling QE3: "QEinfinity." If they do my entry is "TARP2."

From Bloomberg:

Now let's compare apples to apples.

Post a chart showing the 2013 US GDP growth estimate to the 2013 S+P 500 estimate. Or, alternatively, post a chart showing the actual 2013 GDP vs the actual 2013 S+P 500. Of course you'd have to start your Y axis at zero; anything else would be misleading and intellectually dishonest, and I know you'd never stoop to such things.

From Bloomberg:

LOL, that is good. If it is from Bloomberg as you say, then why is your source not Bloomberg? Instead chart is on a whacko nut job conspiracy web site. Actually what you posted is a modification of a chart tweeted by a Bloomberg employee. Below is the actual chart, notice there are some significant differences. And just what malevolence do you find in the chart exactly?

https://twitter.com/M_McDonough/status/364429430841569281/photo/1/large

The estimates have consistently under estimated actual real GDP growth.

http://www.bea.gov/

Probably for same reason, despite being asked more than dozen times in different posts, for the link to Bloomberg, you could never produce one for this "quote of Bloomberg"you made:LOL, that is good. If it is from Bloomberg as you say, then why is your source not Bloomberg? ...

I.e. both you and he just pulled it out of your dark and smelly place where the sun "don't shine."{from joepistole's post here: http://www.sciforums.com/showthread.php?136309-Tapering-the-Taper&p=3125173&viewfull=1#post3125173};

according to Bloomberg, the gold transfer will be completed in 3 years per Germany's request and all parties have agreed to the transfers. ...

Probably for same reason, despite being asked more than dozen times in different posts, for the link to Bloomberg, you could never produce one for this "quote of Bloomberg"you made:I.e. both you and he just pulled it out of your dark and smelly place where the sun "don't shine."

LOL, a little desperate these days are you? How about surprising me one day and make some sense.

Fed's plans:* As I predicted at least 6 years ago.

** Because so many are getting discouraged and ceasing to look more for a job (see rapidly falling labor force participation graph of prior post) the Fed is in danger that its criteria for ending QEs will be met before it is safe (not very destructive to the economy) to begin the tapering. One solution to that is for example lower the 6.5% goal post to say 5.0%. Another is to offset the QEs ending with something that effectively also prints new money etc. but has a different name. - Called above "alternative actions."

Perhaps Fed should hold a name contest with $1000 prize for the winner? I don't think Fed is happy that many of us are calling QE3: "QEinfinity." If they do my entry is "TARP2."

This has been discussed with you and proven many times. But both you and Michael have a knack for ignoring facts. Workforce participation rates are changing because the workforce is changing. The workforce is aging and as a result a lot of people are pulling out of the workforce. It has nothing to do with the Fed.

Only partisans are calling it QE infinity. You won’t find savvy investors who are that stupid. Every day the market fears the ending of QE not for the nefarious reasons you are pushing but because investors are not confident the Fed will get the timing right. And they have good reason for that fear. Historically the Fed has tended to error on the conservative side and end QE early which could cause stagnation or another recession.

Unfortunately for you the BLS does track discouraged workers. They are not growing in number as you like to claim.

“Among the marginally attached, there were 815,000 discouraged workers

in October, essentially unchanged from a year earlier. (The data are

not seasonally adjusted.) Discouraged workers are persons not

currently looking for work because they believe no jobs are available

for them.” BLS, November 2013

And do you really think Wall Street wouldn’t notice your “name change” notion? Further there is no reason for the Fed to change its stated unemployment targets. The unpleasant fact for you is the Fed is doing swimmingly well. And it the numbers show it. You have been sounding the doom and gloom message for years now, you have consistently used conspiracy ads and websites upon which to base your illogical and counterfactual notions. And this year you have committed to predicting a collapse of the dollar, a monetary and economic Armageddon resulting from the actions taken by the Fed. In other words, you are going to have a lot of egg on your face come October of next year when that event fails to materialize. The only hope you have of an economic Armageddon next year is if Republicans in the House intentionally run the nation into a default.

I know as asked you more than a dozen times for link to Bloomberg you claimed to be quoting. Anyone can look at the next 20 of so posts to see you duck and weave, attack me and my sources, but NEVER give the link.This has been discussed with you ...

I know as asked you more than a dozen times for link to Bloomberg you claimed to be quoting. Anyone can look at the next 20 of so posts to see you duck and weave, attack me and my sources, but NEVER give the link.

LOL, do you really want to go there? Apparently you need a memory refresher Billy T. You claimed that the Federal Reserve told Germany it would have to wait 7 years in order to get its gold back from the Federal Reserve and you went on to speculate that The Federal Reserve didn't have the gold because it lent it out to unspecified borrowers and that was the reason for the Fed's delay in returning Germany's gold. And you went on to write that the Fed could just put the gold on an airplane and return all 300 tons of gold within weeks were it not for some nefarious reasons like not having the gold. You further stated that the Federal Reserve had not audited its gold reserve for decades which was false. The Fed completed a gold audit as recently as last year. I pointed out your errors of fact and gave you links and materials to prove you were wrong on all accounts. And I further pointed out your total reliance on known specious conspiracy web sites.

I repeatedly challenged you to produce even one credible source which backed up your claim that the Federal Reserve told Germany it would have to wait 7 years in order to get its gold back as you claimed. You have yet to produce that proof. I on the other hand produced proof of everything. Your obfuscation and refusal to recognize credible evidence from credible sources does not nullify reality. You were challenged a dozen times to provide credible evidence to support your claim the US told Germany it couldn't have it's gold back immediately and must wait 7 years in order to get its gold and as of today you have failed to produce that credible evidence. Because it exists only in your mind and those of your fellow conspiracists. And since then you have nothing but continue to obfuscate. You and Michael have a lot in common, you ignore facts and evidence you find displeasing.

QE Tiger by the tail:

* Especially with the just announced (by Paul Ryan & Patty Murray) new version of "kick the can down the road" that hopes to cause borrowing to increase by "ONLY" 1.01 TRILLION dollars this just starting fiscal year. Not fooling all with hints of significant tapper this December meeting. Perhaps a small one needed to kill the growing realization of the problem - reflected by three down days on Wall street and three up days for gold.

BTW 1: on Joe's false statement at start of post 652:I did not claim it would take 7 years to give Germany back it gold. I QUOTED two different sources (giving their links of course) stating that. Joe rarely can give sources for his "quotes'" and still refuses to give any link to his quote of Bloomberg that he claims contradicts my two sources. I guess Joe thinks LOL and attack other's sources servers as well. I added my comments to effect that if US actually had the unencumbered gold to give back, they could do that in a few months with large US Air Force cargo planes (they can lift several heavy tanks)

BTW 2: As normally Joe's practice is to attack my sources, I note the Wall Street Journal, has operational control over Market Watch and it's Stock Market Quotes, Business News and Financial News from the leading provider: MarketWatch.com, a wholly-owned subsidiary of Dow Jones & Company, Inc.

#3 is a very light load: president's limousine and some secret service cars.

#3 is a very light load: president's limousine and some secret service cars.

#2 is the 82nd Airborne paratroopers seated with their gear for a drop.

#1 Is transport of heavy howlers to Afghanistan. (The length of gun barrel limits them to 2 per trip, not their weight, which is more than heavy tank. I can't find photo of three tanks inside.)

Next post, 653, has photo of just a routine training mission over the Appalachian mountains at low level. Less than half these planes on that training missions could deliver ALL the German gold to Frankfurt less than 12 hours! Proof in next post. CONTRAST MY SOILD PROOF WITH JOE's TOTAL ABSENCE OF ANY!

US Air force only has 223 of the C-17 but if can't spare a few for hauling German Gold, they have been sold in large volumes to more than dozen friendly nations.

http://www.marketwatch.com/story/central-banks-will-move-goal-posts-to-keep-qe-forever-2013-12-11 said:There is only one thing that really matters to the markets. And that is whether central banks will continue with quantitative easing and stick with interest rates at three-century lows — and if not, when they will stop printing money and get rates back to something close to normal levels. In the U.K., rates were meant to start going up when the unemployment rate dropped to 7%. In the U.S., the Federal Reserve targeted a 6.5% jobless rate. But now the Bank of England is looking at rising real wages as a potential trigger for rates to get back to normal, while the Fed is discussing shifting its target from 6.5% unemployment to 6% or else when an inflation floor has been hit.

The U.K. economy has had a stronger bounce back than the bank or anyone else expected. In the third quarter alone, it expanded at 0.8%, the fastest rate among major industrial nations. Given that the U.K. is also good at creating lots of low-paying jobs (although unfortunately not the high-paying sort), unemployment has come down faster than forecast. The latest monthly figures showed unemployment dropping to 7.6% from 7.8%: at that pace, rates will be going up before next spring.

So what does the bank do? It has started making noises about how the 7% target is not set in stone. Instead, it will look at other factors, such as what is happening to real wages, or the rate of productivity growth, before tightening monetary policy.

Much the same thing is happening in the U.S: Back in May, Fed Chairman Ben Bernanke suggested a 7% or 6.5% unemployment rate would be a good moment to start getting monetary policy back to normal. Now 7% is here, and there is still no sign of it. Last month, two papers by a pair of Fed officials discussed whether 6.5% was not a little on the high side, and suggested a 6% target instead . Another paper this month has suggested an “inflation floor” could be the trigger instead: that would rule out any rate hikes until inflation was up to 2% or even 1.5%.

Just like the Bank of England, the {US} central bank set out a pair of clear goal posts, then quickly moved them as soon as there was any chance of the target actually being reached. ... Once you slash interest rates to close on zero it is very hard to get them back up again. Likewise, once you turn on the printing presses, it is incredibly difficult to stop them. History is the best guide, and its lesson could hardly be clearer. Japan cut its interest rates to 0.5% all the way back in September 1995. Nearly two decades later, they still haven’t gone back up again. Nor will they any time soon — in fact, the Bank of Japan keeps on chucking more and more stimulus at the economy.

The U.S., the U.K., or indeed the euro zone, now that it has got its rates down to record lows as well, will not be any different. Why should they? There is very little sign of inflation taking off — in fact, in most of the world it is coming down. Asset bubbles might be popping up all over the place, but if central bankers worried about those they have not shown any sign of it yet. Meanwhile, near-zero rates have long since stopped being an “emergency measure” and have become the new normal.

They are embedded in the economy. The rate rises that would get them back to “normal” are simply too extreme. Companies have issued billions in bonds, mortgages have been taken out, and governments have run up vast deficits, on which they are paying 2% interest or less. Is it really possible to triple all those payments without creating a wave of bankruptcies, repossessions and massive cuts in public spending? Of course not.*

Central banks set a target for getting rates back to normal, then promptly shift it.

The main priority for central bankers such as Mark Carney and Janet Yellen over the next couple of years will be finding fresh excuses for shifting the target again. Rates will rise once husbands always remember their wedding anniversaries. QE will be “tapered” once children go to bed on time. ... The trick will be to find something so unlikely, there is no chance of the target ever being met — because the reality is once rates have been at 0.5% for five years it is impossible to ever get them back to normal.

* Especially with the just announced (by Paul Ryan & Patty Murray) new version of "kick the can down the road" that hopes to cause borrowing to increase by "ONLY" 1.01 TRILLION dollars this just starting fiscal year. Not fooling all with hints of significant tapper this December meeting. Perhaps a small one needed to kill the growing realization of the problem - reflected by three down days on Wall street and three up days for gold.

BTW 1: on Joe's false statement at start of post 652:I did not claim it would take 7 years to give Germany back it gold. I QUOTED two different sources (giving their links of course) stating that. Joe rarely can give sources for his "quotes'" and still refuses to give any link to his quote of Bloomberg that he claims contradicts my two sources. I guess Joe thinks LOL and attack other's sources servers as well. I added my comments to effect that if US actually had the unencumbered gold to give back, they could do that in a few months with large US Air Force cargo planes (they can lift several heavy tanks)

BTW 2: As normally Joe's practice is to attack my sources, I note the Wall Street Journal, has operational control over Market Watch and it's Stock Market Quotes, Business News and Financial News from the leading provider: MarketWatch.com, a wholly-owned subsidiary of Dow Jones & Company, Inc.

#2 is the 82nd Airborne paratroopers seated with their gear for a drop.

#1 Is transport of heavy howlers to Afghanistan. (The length of gun barrel limits them to 2 per trip, not their weight, which is more than heavy tank. I can't find photo of three tanks inside.)

Next post, 653, has photo of just a routine training mission over the Appalachian mountains at low level. Less than half these planes on that training missions could deliver ALL the German gold to Frankfurt less than 12 hours! Proof in next post. CONTRAST MY SOILD PROOF WITH JOE's TOTAL ABSENCE OF ANY!

US Air force only has 223 of the C-17 but if can't spare a few for hauling German Gold, they have been sold in large volumes to more than dozen friendly nations.

Last edited by a moderator:

LOL, ... {a false statement here removed as replied to near end of prior post} ... And you went on to write that the Fed could just put the gold on an airplane and return all 300 tons of gold within weeks were it not for some nefarious reasons like not having the gold. You further stated that the Federal Reserve had not audited its gold reserve for decades which was false. {That is another false statement: I said the last audit of the Fed was more than six decades ago and even then not fully independently done. I don't know if the fox has audited the hen house since then. Ron Paul tried for years to get a new audit done.}...

US has 223 C-17s and these 12 friendly nations have more than 100.

The C-17 makes the NYC to Frankfurt trip in less than 7 hours, including take-off and landing time. They can carry more than 160,000 pounds for these short trips, but lets say they only take 80 tons per trip.http://www.heavyairliftwing.org/library/c-17-aircraft/boeing-c-17-aircraft-fact-sheet said:Range with Payload: 160,000 pounds 2,500 nautical miles Cruise Speed 0.74 - 0.77 Mach {= >591miles /hour}

300 tons / 80 tons per trip is less than four trips. One third of the C-17s seen below on training mission could return ALL of Germany's gold in 12 hours. I.e.

There is some other reason why German can't get it gold back NOW. . . Can you guess what it is?

** Germany has twice sent members of their audit committee to gold vault in NYC. First time not even taken to vault. Second time allowed to look thru door, not allowed touch an ounce!

SUMMARY:

LIKE USUSAL , JOE POSTS HIS BULL SHIT AND CLAIMS TO BE QUOTING RELIABLE SOURCE, LIKE BLOOMBERG, but even after ~15 requests for link to it, all you get is: "LOL"

Last edited by a moderator:

3852 miles NYC to Frankfurt, Germany.

3852 miles NYC to Frankfurt, Germany.

US has 223 C-17s and these 12 friendly nations have more than 100.The C-17 makes the NYC to Frankfurt trip in less than 7 hours, including take-off and landing time. They can carry more than 160,000 pounds for these short trips, but lets say they only take 80 tons per trip.

300 tons / 80 tons per trip is less than four trips. One third of the C-17s seen below on training mission could return ALL of Germany's gold in 12 hours. I.e.

There is some other reason why German can't get it gold back NOW. . . Can you guess what it is?

My guess: (and that of many others) is US either does not have their gold** (why no audit allowed) or has lent the gold out long term for income.

** Germany has twice sent members of their audit committee to gold vault in NYC. First time not even taken to vault. Second time allowed to look thru door, not allowed touch an ounce!

SUMMARY:

LIKE USUSAL , JOE POSTS HIS BULL SHIT AND CLAIMS TO BE QUOTING RELIABLE SOURCE, LIKE BLOOMBERG, but even after ~15 requests for link to it, all you get is: "LOL"

My challenge remains unanswered Billy T. Where is your credible evidence to support your claim that The Federal Reserve told Germany it would have to wait 7 years to get its gold back?

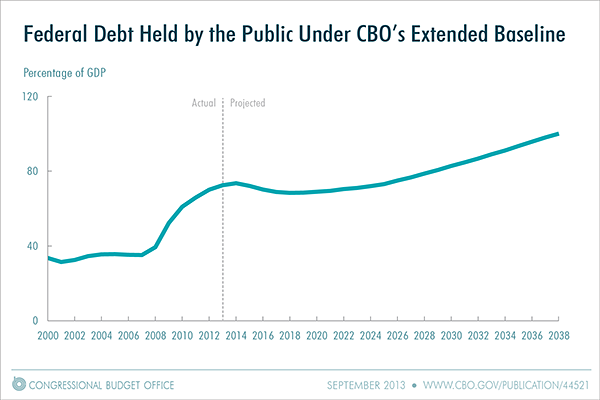

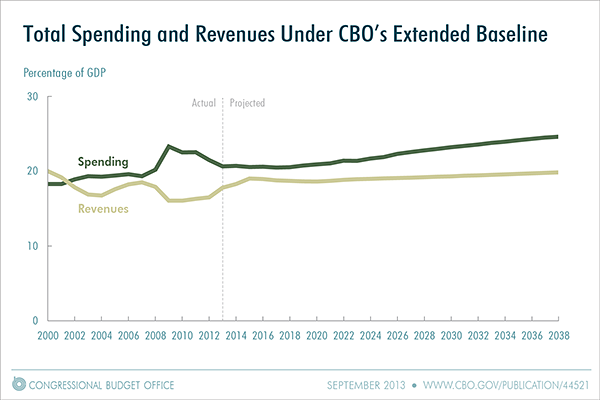

That 2nd graph deficit gap adds to the growing debt and becomes ever harder to carry, especially as interest rates return to even near historical averages.

PS to Joe: I gave two DIFFERENT links that said US would require 7 years to give Germany all its gold back. It is not my fault that you don't want to consider them "creditable." At least I do give links for my quotes. You just claimed to be quoting Bloomberg saying it goes back in 3 years, but NEVER give the link, even after about 15 requests for it.

SUMMARY: You can add that to your long list of fabricated lies that a dozen relies of your "LOL" or duck and weave attacks on me will not wash out - only the link will.

My challenge remains unanswered Billy T. Where is your credible evidence to support your claim that The Federal Reserve told Germany it would have to wait 7 years to get its gold back?

QE Tiger by the tail:

* Especially with the just announced (by Paul Ryan & Patty Murray) new version of "kick the can down the road" that hopes to cause borrowing to increase by "ONLY" 1.01 TRILLION dollars this just starting fiscal year. Not fooling all with hints of significant tapper this December meeting. Perhaps a small one needed to kill the growing realization of the problem - reflected by three down days on Wall street and three up days for gold.

BTW 1: on Joe's false statement at start of post 652:I did not claim it would take 7 years to give Germany back it gold. I QUOTED two different sources (giving their links of course) stating that. Joe rarely can give sources for his "quotes'" and still refuses to give any link to his quote of Bloomberg that he claims contradicts my two sources. I guess Joe thinks LOL and attack other's sources servers as well. I added my comments to effect that if US actually had the unencumbered gold to give back, they could do that in a few months with large US Air Force cargo planes (they can lift several heavy tanks)

BTW 2: As normally Joe's practice is to attack my sources, I note the Wall Street Journal, has operational control over Market Watch and it's Stock Market Quotes, Business News and Financial News from the leading provider: MarketWatch.com, a wholly-owned subsidiary of Dow Jones & Company, Inc.

#3 is a very light load: president's limousine and some secret service cars.

#2 is the 82nd Airborne paratroopers seated with their gear for a drop.

#1 Is transport of heavy howlers to Afghanistan. (The length of gun barrel limits them to 2 per trip, not their weight, which is more than heavy tank. I can't find photo of three tanks inside.)

Next post, 653, has photo of just a routine training mission over the Appalachian mountains at low level. Less than half these planes on that training missions could deliver ALL the German gold to Frankfurt less than 12 hours! Proof in next post. CONTRAST MY SOILD PROOF WITH JOE's TOTAL ABSENCE OF ANY!

US Air force only has 223 of the C-17 but if can't spare a few for hauling German Gold, they have been sold in large volumes to more than dozen friendly nations.

That is hogwash Billy T. Where is the evidence to support your claim the Federal Reserve told Germany it couldn't have its gold back right away and would need to wait 7 years and suggesting that the Fed didn't have the gold?

Additionally you are abusing your power as a moderator. You are revising history, posts, lying and you have taken to limiting my ability to post in this thread.

First, for 2nd or 3d time: Not my claim - just my quote from two different sources, but there is supporting indications, two of which I soon mention and then give you a question in bold type.That is hogwash Billy T. Where is the evidence to support your claim the Federal Reserve told Germany it couldn't have its gold back right away and would need to wait 7 years and suggesting that the Fed didn't have the gold?

I.e. I gave two different links and quoted from them telling the seven years needed for return of all Germny's gold.

Also contrary to your claim that it would take long time to return 300 tones, I gave in last few posts complete proof that four (or 6 each with 50 tons and more fuel. then refueling by KC 135 might not even be required, but it is routine. See photo below.) C-17s could deliver it to Frankfurt* in less than 12 hours. Fact it has been nearly a year since Germany asked for it gold back plus the fact that twice Germany audit committee representatives were not even allowed to touch their gold, certainly lends strength to the idea that US does not have unencumbered gold to give back now. Why do you think it has not all been returned months ago?

* See post 653 & 654 for detail, including photos, one showing 13 of the 223 C-17s the US owns in training mission flight.

You need to learn that personal attacks and "LOL" are not rebuttals to well documented facts (like about the C-17's lift capacity, speed and range with 80 tones of cargo) and referenced information quoted from other sourceS.

Another set of lies! I have power to block post by new (less than 20 post made) members. Please PM James R and ask him to look at the past archives for any evidence that you have had any post blocked by me or stop inventing more lies.you are abusing your power *as a moderator. You are revising history, posts, lying and you have taken to limiting* my ability to post in this thread.

* If I even have that power, which I don't, I would not know how to use it.

I'm not saying following quote is true / correct, but it does help explain why the price of "paper gold" has fallen despite physical gold demand and buying being greater than total global production (excluding China who never lets any of its production leave China but is buying ~1200 ton in the western markets in 2013):

I know you will just, as you normally do, attack the credibility of the source rather than discuss the logic or supporting evidence. - Especially the strange fact that the law of supply demand normally causes prices to rise rather than fall when demand exceeds production. Also, Goldman Sucks has been convicted of going short for it own account when telling others to buy and other efforts at market manipulation are at least widely suspected by these banks with large gold account holdings, both long and short.http://www.reddit.com/r/conspiracy/comments/1fao91/somebody_is_messing_with_the_gold_market/ said:part of the equation is that Germany is repatriating its gold from WWII. Problem is, the US has lent it out and cannot return it yet. So they have to use Goldman Sachs and JP Morgan to push the gold market down to make gold cheaper to buy back.

Last edited by a moderator:

This IS the recovery.

We're living it.

So, if you think life is pretty good - then that's great. It's only going down from here.

I would guess the Federal Reserve will begin another attempt at a tapper in 2014 - and this 'recovery' will be the New Normal. Everyone will adjust to it as that's what people do, normalize.

I predict in our lifetimes we'll see another normalization to middle class parents putting their children into part-time work to help with the rent and bills. Then, children working will be seen as 'good for society' and therefor 'good for kids. Onwards we'll 'progress' until we've 'progressed' right back into a third world shit-hole most inner cities presently are (See: Detroit).

We're living it.

So, if you think life is pretty good - then that's great. It's only going down from here.

I would guess the Federal Reserve will begin another attempt at a tapper in 2014 - and this 'recovery' will be the New Normal. Everyone will adjust to it as that's what people do, normalize.

I predict in our lifetimes we'll see another normalization to middle class parents putting their children into part-time work to help with the rent and bills. Then, children working will be seen as 'good for society' and therefor 'good for kids. Onwards we'll 'progress' until we've 'progressed' right back into a third world shit-hole most inner cities presently are (See: Detroit).

I'd give a modest $5billion reduction this week a 50/50 chance. - Fed just wanting to show it can reduce the buying with thin-air money below the 1 trillion per year rate. I.e. Fed keeps firm hold on the tiger's tail, with a move of slight psychological, no fiscal, significance.... I would guess the Federal Reserve will begin another attempt at a tapper in 2014 ...